Plot Ridge coefficients as a function of the L2 regularization¶

Ridge Regression is the estimator used in this example.

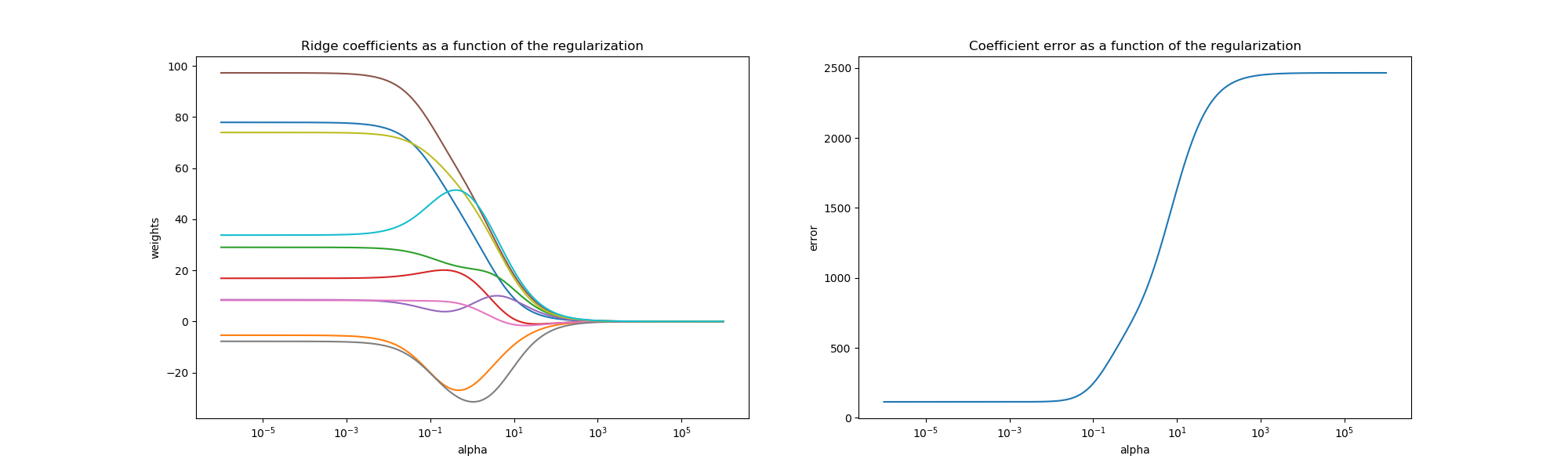

Each color in the left plot represents one different dimension of the

coefficient vector, and this is displayed as a function of the

regularization parameter. The right plot shows how exact the solution

is. This example illustrates how a well defined solution is

found by Ridge regression and how regularization affects the

coefficients and their values. The plot on the right shows how

the difference of the coefficients from the estimator changes

as a function of regularization.

In this example the dependent variable Y is set as a function of the input features: y = X*w + c. The coefficient vector w is randomly sampled from a normal distribution, whereas the bias term c is set to a constant.

As alpha tends toward zero the coefficients found by Ridge regression stabilize towards the randomly sampled vector w. For big alpha (strong regularisation) the coefficients are smaller (eventually converging at 0) leading to a simpler and biased solution. These dependencies can be observed on the left plot.

The right plot shows the mean squared error between the coefficients found by the model and the chosen vector w. Less regularised models retrieve the exact coefficients (error is equal to 0), stronger regularised models increase the error.

Please note that in this example the data is non-noisy, hence it is possible to extract the exact coefficients.

# Author: Kornel Kielczewski -- <[email protected]>

print(__doc__)

import matplotlib.pyplot as plt

import numpy as np

from sklearn.datasets import make_regression

from sklearn.linear_model import Ridge

from sklearn.metrics import mean_squared_error

clf = Ridge()

X, y, w = make_regression(n_samples=10, n_features=10, coef=True,

random_state=1, bias=3.5)

coefs = []

errors = []

alphas = np.logspace(-6, 6, 200)

# Train the model with different regularisation strengths

for a in alphas:

clf.set_params(alpha=a)

clf.fit(X, y)

coefs.append(clf.coef_)

errors.append(mean_squared_error(clf.coef_, w))

# Display results

plt.figure(figsize=(20, 6))

plt.subplot(121)

ax = plt.gca()

ax.plot(alphas, coefs)

ax.set_xscale('log')

plt.xlabel('alpha')

plt.ylabel('weights')

plt.title('Ridge coefficients as a function of the regularization')

plt.axis('tight')

plt.subplot(122)

ax = plt.gca()

ax.plot(alphas, errors)

ax.set_xscale('log')

plt.xlabel('alpha')

plt.ylabel('error')

plt.title('Coefficient error as a function of the regularization')

plt.axis('tight')

plt.show()

Total running time of the script: ( 0 minutes 0.203 seconds)